The Canada Strong Fund: Sovereign Leverage, Not Sovereign Wealth

Canada has announced its first national SWF. The name is the least of its problems.

Mark Carney understands capital. That makes the Canada Strong Fund announcement at the end of April even more curious. What Carney unveiled is not, by my definition, a Sovereign Wealth Fund. It is a government investment vehicle [debt-financed and politically motivated] dressed in the language of nation-building. More precisely: it is a Sovereign Leverage Fund. In a country that has already resolved this question at the provincial level, the federal experiment raises a harder question than it answers.

Multiple Mandates, no clear Direction

The Canada Strong Fund wants to inhabit all four corners of the sovereign wealth taxonomy simultaneously; a “quasi Super Fund”. It is a stabilisation vehicle, state-owned enterprise Holdco and a strategic development fund.

Saudi Arabia’s Public Investment Fund attempted a comparable consolidation of mandates and has spent years managing the governance tensions that result. Canada does not have Saudi Arabia’s revenue base, its political consensus mechanisms, or its fiscal surplus. It is starting from a more constrained position and attempting a more ambitious mandate.

The Fund is trying to be a sovereign wealth fund, a development bank, a commercial investor, an industrial policy vehicle and a retail savings product at the same time. No single institution runs on five mandates. Mandate clarity is the first line of defence against a fund becoming a vehicle for political allocation rather than economic return. This is no 1MDB, but multiple mandates run the risk of leakage, inefficiency and frankly, unperforming returns.

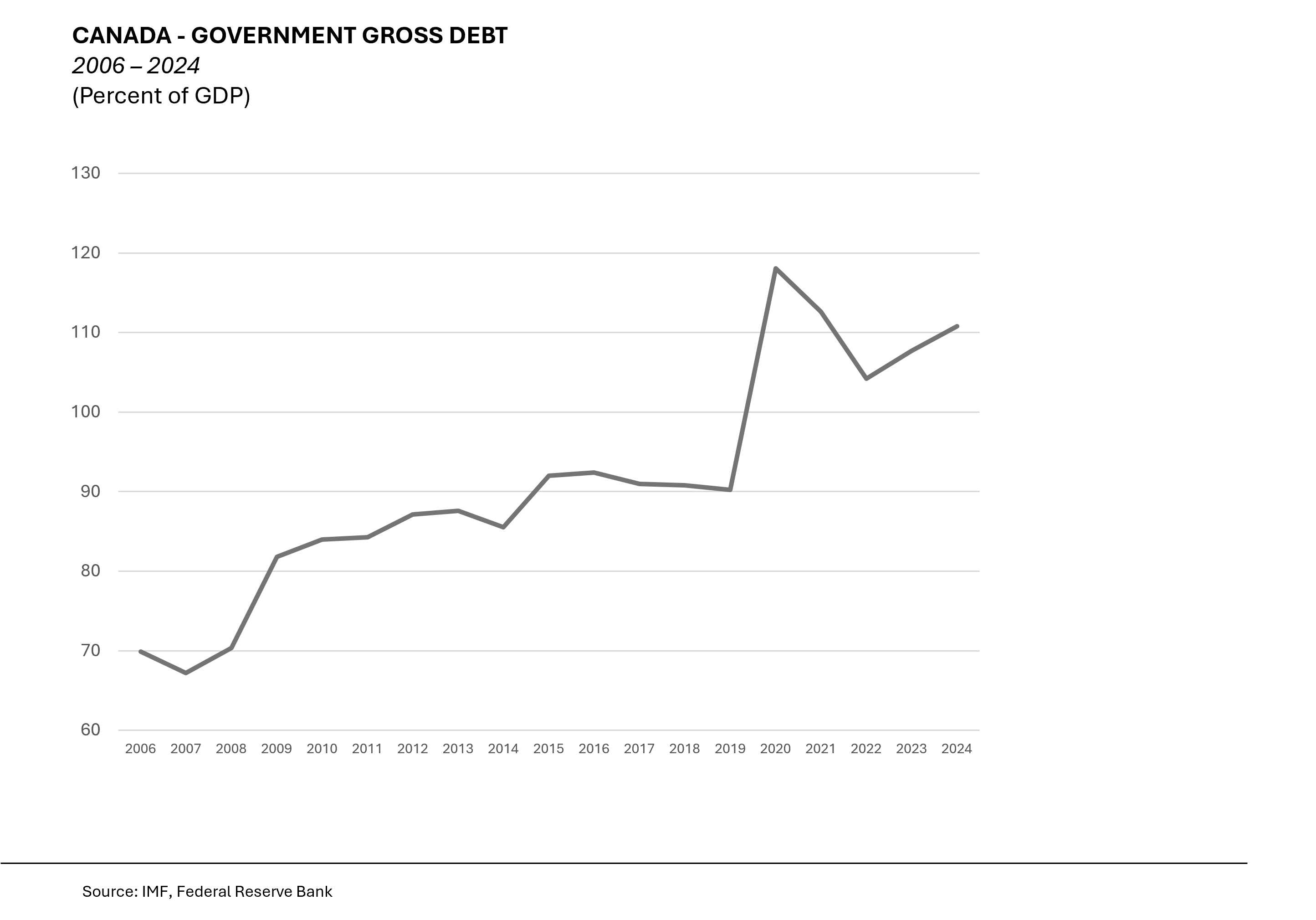

Canada’s Fiscal Position: The Debt Picture

The government’s framing of Canada’s fiscal strength deserves scrutiny. Canada’s net debt-to-GDP ratio of 10.2% compares favourably within the G7, but net debt and the trajectory of gross debt are different concepts; the trajectory is what matters for a fund capitalized entirely by borrowing.

The data clarifies the challenge. Federal gross debt-to-GDP peaked at 118% of GDP in 2020 during the pandemic, falling to approximately 107% by 2022-23 before rising again to around 111% in 2024. The Spring Economic Update 2026 projects the current-year deficit at CAD 66.9 billion, 2.1% of GDP. The Parliamentary Budget Officer has noted that under Budget 2025’s fiscal plan, deficits are projected to average CAD 64.3 billion annually through to 2029-30, more than double the pre-pandemic average. Debt servicing costs already consume 10.5 cents / revenue dollar, up from 5.9 cents in 2021-22 and are projected to rise to CAD 76 billion annually by 2030.

Canada is not drawing on accumulated savings to build this fund. It is borrowing to build what Norway saved to create. That distinction is not semantic but defines the entire risk profile of the enterprise.

The Cost of Capital Contradiction

This is the structural fault line at the centre of the Canada Strong Fund. Every dollar deployed carries a cost: Canada’s sovereign borrowing rate on the bonds issued to capitalise it. For the Fund to justify its existence commercially, portfolio returns must exceed that borrowing rate. If they merely match it, Canadians bear investment risk and receive nothing for it. If they fall short, the Fund destroys value.

The government has committed to “strong, commercial returns” but has not specified the return threshold required to clear the cost-of-capital hurdle. The sectors identified are clean and conventional energy, critical minerals, nuclear, high-speed rail; all capital-intensive, long-duration and politically complex. Many are unlikely to generate market rates of return on any conventional analysis in the mid term.

This creates an inescapable logical trap. Canada has a deep banking system, pension funds managing over CAD 2.6 trillion in assets, private equity and an existing suite of public financing institutions. Alongside this new fund, there is the Canada Infrastructure Bank, the Canada Growth Fund, Export Development Canada and the Business Development Bank of Canada. If a project clears a commercial return hurdle above the government’s borrowing rate, one of these institutions should already take up the mandate. If none of them are, the most likely explanation is that the project does not clear that hurdle. The Canada Strong Fund does not resolve this problem. It reframes it under a new name.

The Political Economy Problem: Federalism as a Structural Constraint

Here is the deeper issue that the sovereign wealth framing obscures; Canada has already answered the question of how to manage resource-derived public capital and the answer is at a provincial level.

Alberta’s Heritage Savings Trust Fund manages CAD 31.9 billion, capitalised by provincial resource royalties that Alberta controls. Quebec’s Generations Fund manages a distinct model blending sovereign and quasi-pension capital with domestic industrial mandates. Newfoundland and Labrador and the Northwest Territories each operate their own resource-backed vehicles. Every one of these funds draws on revenues the respective province constitutionally controls. On balance sheet, none are debt-financed.

The federal government cannot replicate this model because Canadian constitutional architecture routes natural resource royalties to the provinces, not Ottawa. This is not a policy failure but the political design of the federation. It means the Norway comparison [which Carney himself invoked] is politically and structurally unavailable at a federal level in Canada.

The projects the Fund is intended to finance, such as energy corridors, ports, critical minerals, inter-provincial transportation, are also predominantly matters of provincial regulatory approval, environmental review and land-use authorisation. Federal equity in projects subject to provincial jurisdiction creates even more political pressure with it is debt funded.

This brings us to the most pointed policy question the government has not answered; if the projects in the Canada Strong Fund’s pipeline cannot attract private capital on commercial terms, why does Canada not use the existing PPP framework that is has successfully used for hundreds of projects across the country? The Canada Infrastructure Bank, a vehicle designed to bridge the same public-private financing gap, will now compete with the Canada Strong Fund. If the CIB, with its mandate and capital, cannot move these projects, the addition of a new debt-backed “Fund” does not improve the outcome. The transaction costs, governance overlaps and jurisdictional tensions remain. The only new addition is debt. A quasi-SWF funded by sovereign debt and private co-investment does not change the underlying risk. It redistributes it: onto the federal balance sheet and, ultimately, onto Canadian taxpayers.

Borrowed Capital, Borrowed Time

The language of sovereign wealth carries specific connotations. They have predominantly been driven by a state that has generated surplus, set it aside and committed to deploy it across a long horizon. Norway, Kuwait, Abu Dhabi and Singapore each reflects a deliberate choice to convert resource or trade surpluses into permanent institutional capital. The discipline required to maintain those funds through periods of fiscal pressure is itself a governance achievement.

The Canada Strong Fund may yet develop into something useful. But as announced, it is not a sovereign wealth fund. It is a government borrowing programme, dressed as a wealth vehicle, designed to direct public money toward projects the market has assessed and declined. This is amplified by the fact that it is in a federation where the constitutional architecture, the provincial track record and the existing suite of public financing institutions all point toward a different answer.

Sovereign Wealth Funds are popular in policy circles today. It seems every state is considering why they do not have one already. But a fund that cannot define its mandate, cannot justify its cost of capital and cannot operate successfully in its political economy, is not a Sovereign Wealth Fund. As new tool of nation-building, Canada may build the world’s first Sovereign Debt Fund.